Ace Deferred Tax In P&l

Contoh Laporan Keuangan Lengkap 15 Jenis Perusahaan Pengusaha Consolidated Trial Balance Financial Accounting With Ifrs

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Calculation A Balance Sheet Lists What Goes Under Equity On

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Calculation Accounting For Dividends Declared But Not Paid Ifrs Retained Earnings Profit And Loss Account

Worked Example Accounting For Deferred Tax Assets The Footnotes Analyst Investment Bank Balance Sheet Important Ratios

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition Calculation Profit And Loss Analysis Report Where Is Equity On Balance Sheet

Pin On Mesa Cash Flow Statement Balance Sheet Financial Internal And External Analysis Of Statements From Investing

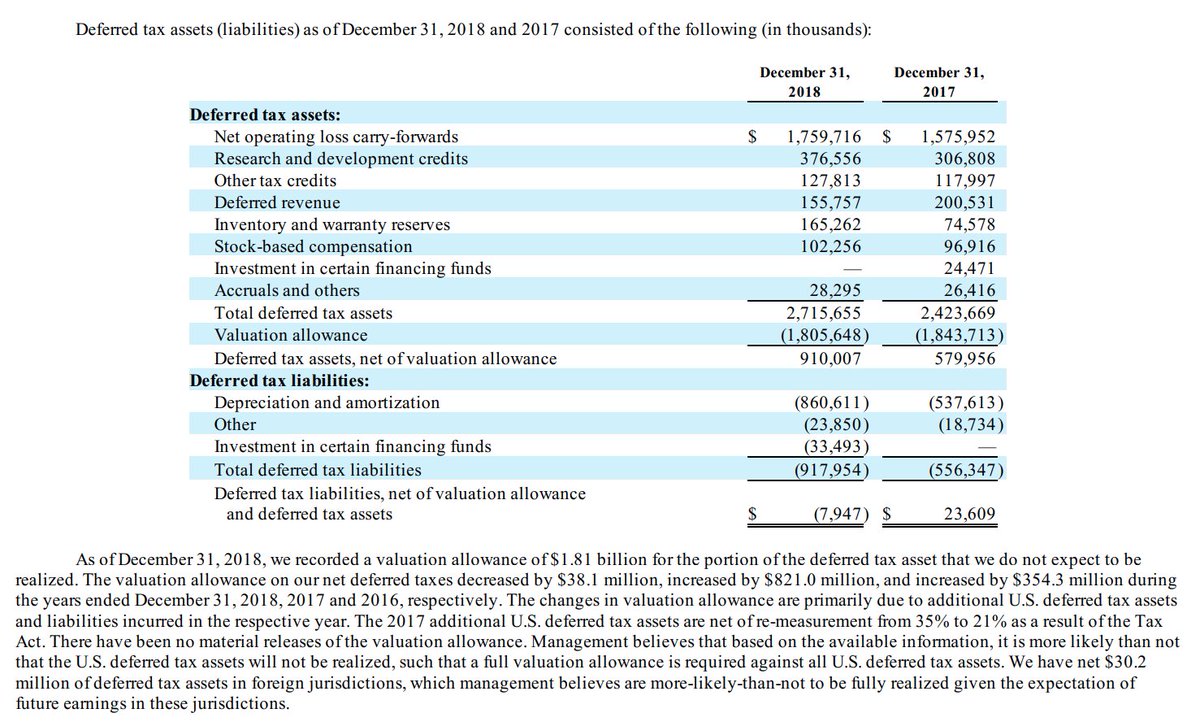

Thus deferred tax is the tax for those items which are accounted in Profit Loss Ac but not accounted in taxable income which may be accounted in future taxable income vice versa.

Deferred tax in p&l. This adjustment made at year-end closing of Books of Accounts affects the Income-tax outgo of the Business for that year as well as the years ahead. Deferred Tax Liabilities or Deferred Tax Liability DTL is the deferment of the due tax liabilities. A deferred tax liability represents an obligation to pay taxes in the future.

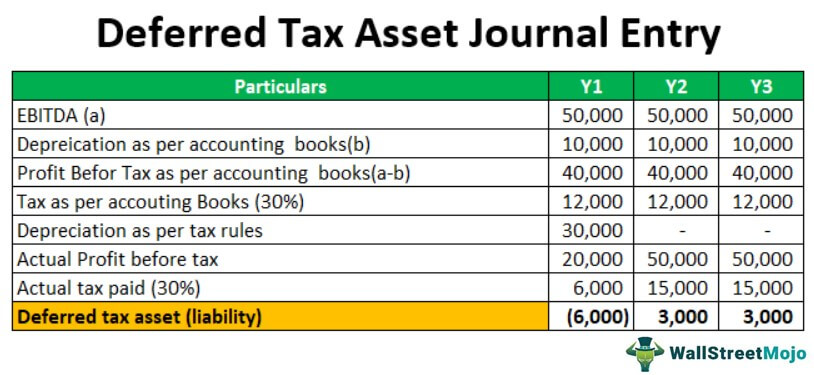

See a simple example below. Try it free for 7 days. The carrying amount of an asset is higher than its tax baseor The carrying amount of a liability is lower than its tax base.

Avoiding pitfalls the manner of recovery and the blended rate 22 Section 5. Deferred taxexpense PL XX Deferred tax balance FP XX Change in tax rate deferred tax consequences If a DTA OBalX decrease in TR Old TR If b DTL OBal X increase in TR Old TR c Opening balance is a deferred tax liability and the tax rate decreases. Calculating a deferred tax balance the basics 3 Section 2.

Deferred tax Deferred tax is a topic that is consistently tested in Paper F7 Financial Reporting and is often tested in further detail in Paper P2 Corporate Reporting. A provision is created when deferred tax is charged to the profit and loss account and this provision is reduced as the timing difference reduces. A deferred tax asset is an item on the balance sheet that results from overpayment or advance payment of taxes.

Avoiding pitfalls share-based payments 33. A deferred tax liability is a liability to future income tax. If different tax rates apply to different levels of taxable profit deferred tax is measured using an average rate s that have been enacted or substantively enacted at the balance sheet date and that will apply to the taxable profit or loss of the periods in which the company expects the deferred tax asset or liability to be realised or settled.

Lets look at an example. Such a difference in tax primarily arises because of the timing difference when the tax is due and when the company pays it. Allocating the deferred tax charge or credit 12 Section 3.

Deferred Tax Asset Journal Entry How To Recognize Aicpa Ssae 16 Prior Year Adjustment Annual Report

Financial Statement Templates 13 Free Word Excel Pdf Of Position Template Accounting For Sale Investment In Subsidiary Simple Balance Sheet

Deferred Tax Asset Journal Entry How To Recognize Financial Ratios For Manufacturing Companies Free Personal Statement Template Excel

Join Profitchain Whatsapp Groups Right Away See Free Verification Of Trades In Real Time Investing Wealth Management Investment Portfolio Cash Flow Analysis Sample Financial Statements For Construction Company

Stray Thoughts Modelling Deferred Tax Assets Or Liabilities Abi Financial Statements Debenture Sinking Fund In Cash Flow Statement

Accounting For Income Taxes Under Asc 740 Deferred Gaap Dynamics Tax Statement 2020 Walmart 2018

Rumus Ekuitas Akuntansi Aquity Beserta Contoh Soal Dan Jawaban Financial Statement Analysis Accounting 3 Year Income Sample Excel

Balance Sheet Profit And Loss Account Under Companies Act 2013 Accounting Taxation Statement Free Cash Flow Direct Method Assets Liabilities Equity