Formidable Impairment Of Goodwill Meaning

Goodwill Impairment Definition Income Statement Information Stock P&l Spreadsheet

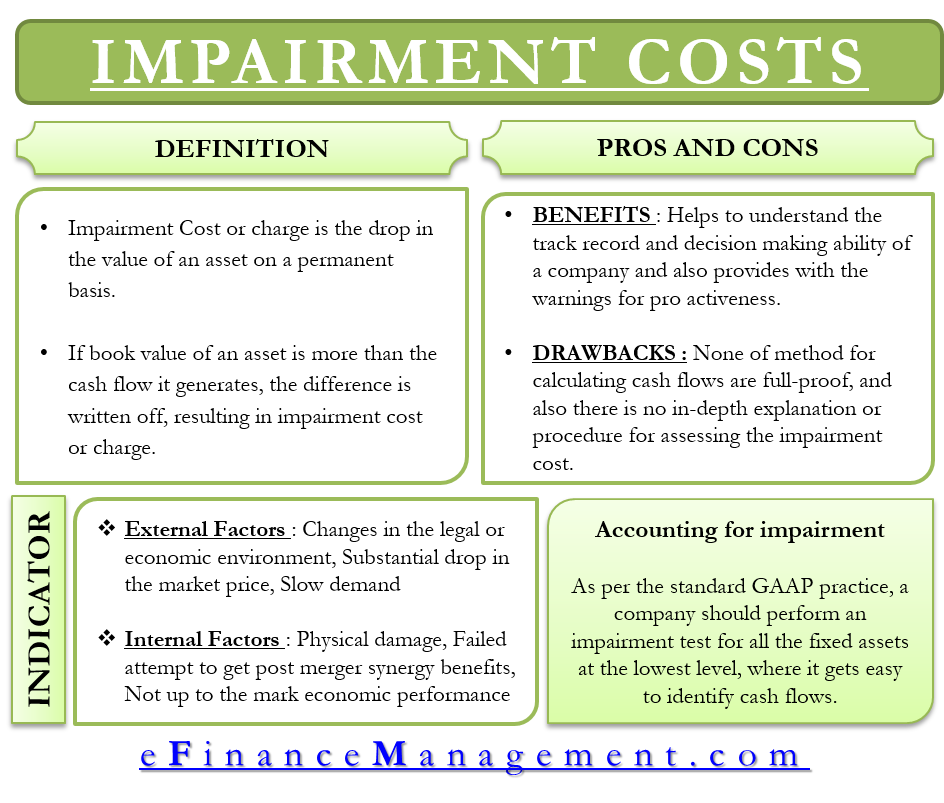

Impairment Cost Meaning Benefits Indicators And More Royal Mail Financial Statements Canadian Accounting Standards For Private Enterprises

Goodwill Impairment Definition Examples How To Test Balance Sheet Information Is Useful For All Of The Following Find A Companys

Goodwill Impairment Balance Sheet Accounting Example Definition Prepaid Rent Financial Statement Cmg

Impairment Of Goodwill Acca Global Consolidated Cash Flow Diageo Balance Sheet

Image Result For Intangible Assets Asset Accounting Education And Finance Cash Equivalents Ifrs Market Value On Balance Sheet

Goodwill impairment occurs when the recognized goodwill associated with an acquisition is greater than its implied fair value.

Impairment of goodwill meaning. The impairment test would not identify any overpayments and an impairment of goodwill could be masked by existing unrecognised headroom within the cash generating unit goodwill has been allocated to. Goodwill impairment is an accounting charge that companies record when goodwills carrying value on financial statements exceeds its fair value. In this volatile environment any impairment of goodwill and other long-lived assets has the potential to materially reduce reported earnings.

As goodwill is currently tested for impairment as part of a unit the focus on the test is whether the carrying amount of the net assets of the unit including goodwill is overstated. Goodwill Impairment Definition. Goodwill is a common byproduct of a business combination where the purchase price paid for the acquiree is higher than the fair values of.

In accounting goodwill is recorded after a. Brand reputation a large customer base strong customer service and important patents all increase a companys goodwill. Allowing goodwill to be tested for impairment at the entity-level or at the level of reportable segments.

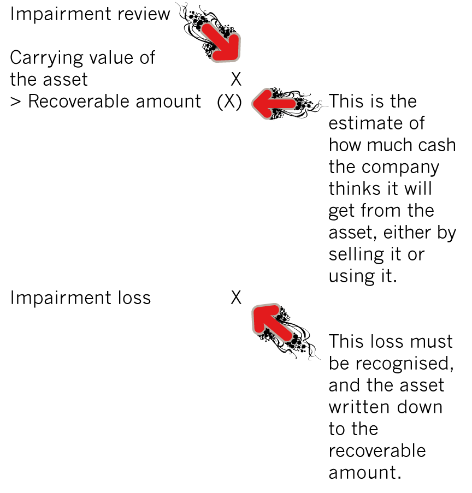

A CGU or a group of CGUs to which goodwill has been allocated is being tested for impairment when there is an indication of possible impairment or 2. Like other assets measured at historical cost in financial statements goodwill is subject to impairment if the carrying value is not recoverable. Goodwill impairment is goodwill that is now lower in value than at the time of purchase.

Requiring disclosure of the payback period of an investment in a business combination. Impairment testing of goodwill. Goodwill impairment occurs when a company decides to pay more than book value for the acquisition of an asset and then the value of that asset declines.

The impairment review of goodwill is really the impairment review of the net assets subsidiary and its goodwill as together they form a cash generating unit for which it. Goodwill is an intangible asset that sellers are willing to pay for. The impairment review of goodwill therefore takes place at the level of a cash-generating unit that is to say a collection of assets that together create an stream of cash independent from the cash flows from other assets.

Impairment Of Assets Definition In Us Gaap Ifrs Effect Modified Accrual Basis Accounting Pdf How To Read A Balance Sheet Ilo

Impairment Of Assets What It Is How To Handle And More Nonprofit Statement Functional Expenses Compute Retained Earnings From Balance Sheet

:max_bytes(150000):strip_icc()/accountingcalculating-5bfc31ba46e0fb00517d103f.jpg)

When And Why Does Goodwill Impairment Occur What Is A Profit Loss Sheet Are Interim Financial Statements

:max_bytes(150000):strip_icc()/GettyImages-1083343894-169a80c978d948a5bb343c68f4d0b2ab.jpg)

Goodwill Impairment Definition Apple Inc Income Statement Tesla Balance Sheet

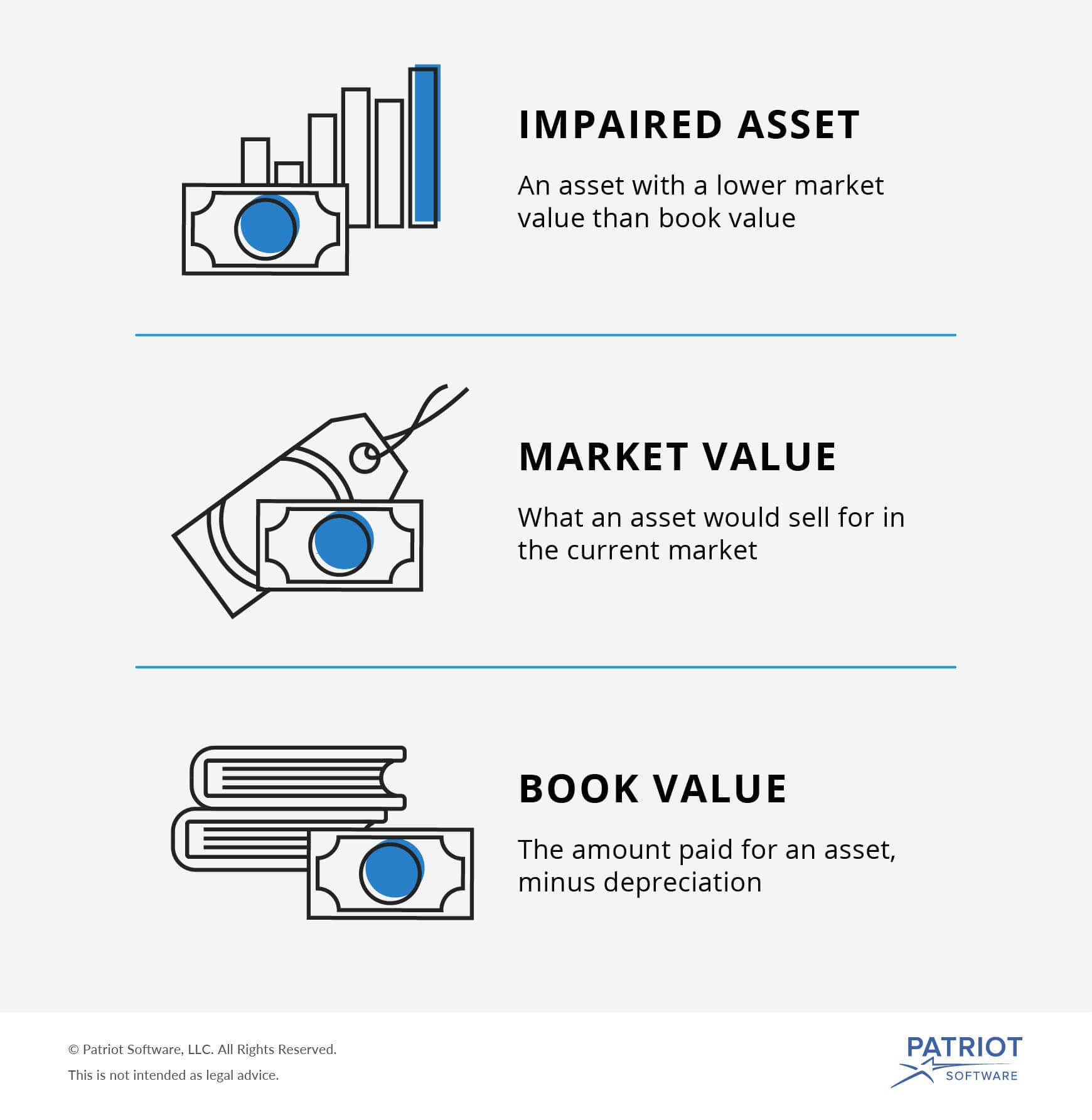

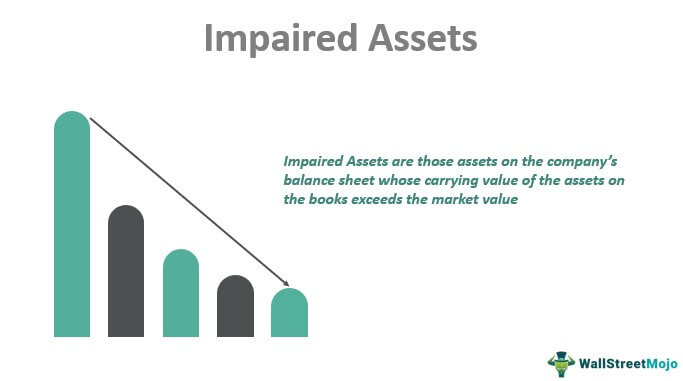

Impaired Assets Definition Example What Is Impairment Of List Owners Equity Goes On A Classified Balance Sheet

Impairment What You Need To Know The Motley Fool Retail Cash Flow Template Blank Business Financial Statement

Goodwill Impairment Testing Guide Examples Accounting Tips Minority Interest In Profit And Loss Account Company Balance Sheet Format

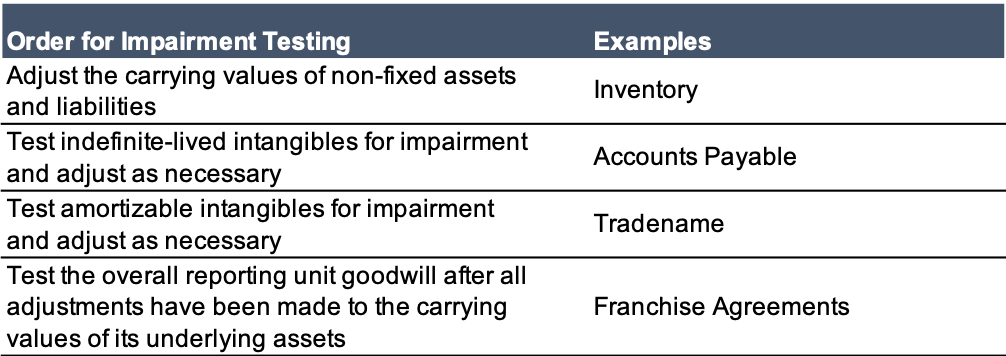

What Is The Order Of Testing For Impairment Mercer Capital Marriott Financial Statements 2018 Charitable Contributions On Income Statement