Casual Disclaimer Of Opinion Going Concern

Adverse Audit Opinion Definition Example Explanation Wikiaccounting Pl Balance Sheet Current Ifrs Standards

Unqualified Opinion Definition Example Vs Qualified Accountinguide Aml Audit Report Solid Financial Position

Topic 9 Reporting Obligations Ppt Download Profit And Loss Other Comprehensive Income Contoh Statement Of Financial Position

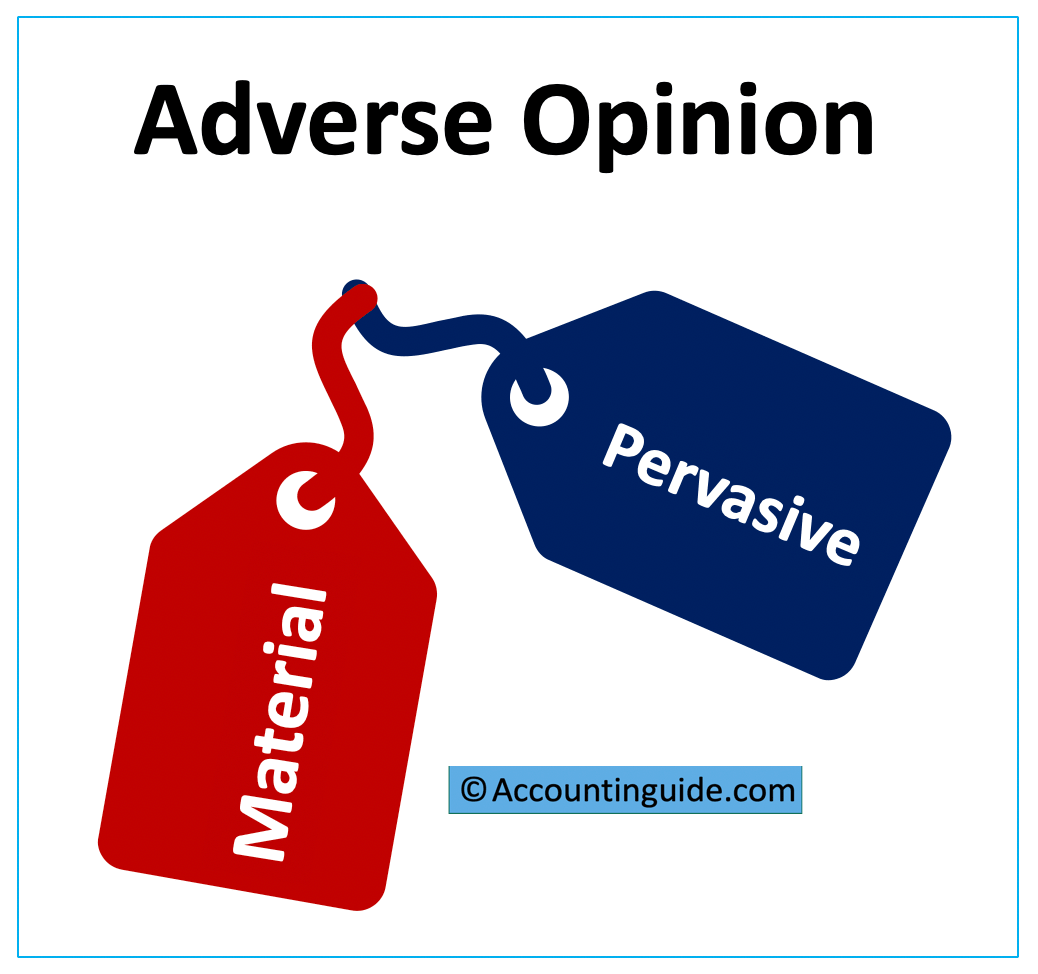

Adverse Opinion Definition Example Vs Disclaimer Accountinguide Financial Ratios And Formulas Institution Audit

Doubt About Going Concern Basis Results In Disclaimer Of Opinion Audit Analyticsaudit Analytics Progressive Insurance Financial Statements Example For Accrued Expenses

Audit Reports Overview Ppt Download Profit And Loss Account Format In Excel Sheet Is Trial Balance A Financial Statement

TH Heavy Engineering Bhds external auditor Deloitte has again issued a disclaimer of opinion on the groups financial statements for the financial year ended Dec 31 2018 FY18.

Disclaimer of opinion going concern. The going-concern assumption GC also known as t he. It is relevant for directors b ecause. Statements do not include the adjustments that would result if the company and the group are unable to continue as going concerns it said.

The underlying issue giving rise to the audit modification has been resolved before the issuer publishes its preliminary results announcement. The auditor is unable. An adverse opinion includes major exceptions or warnings for instance when the auditor believes there are questions whether the firm can remain a going concern A disclaimer of opinion arises if the auditor simply refuses to provide an opinion given limitations on the scope of the audit or if significant material weaknesses in the internal controls and reporting material mean that an opinion.

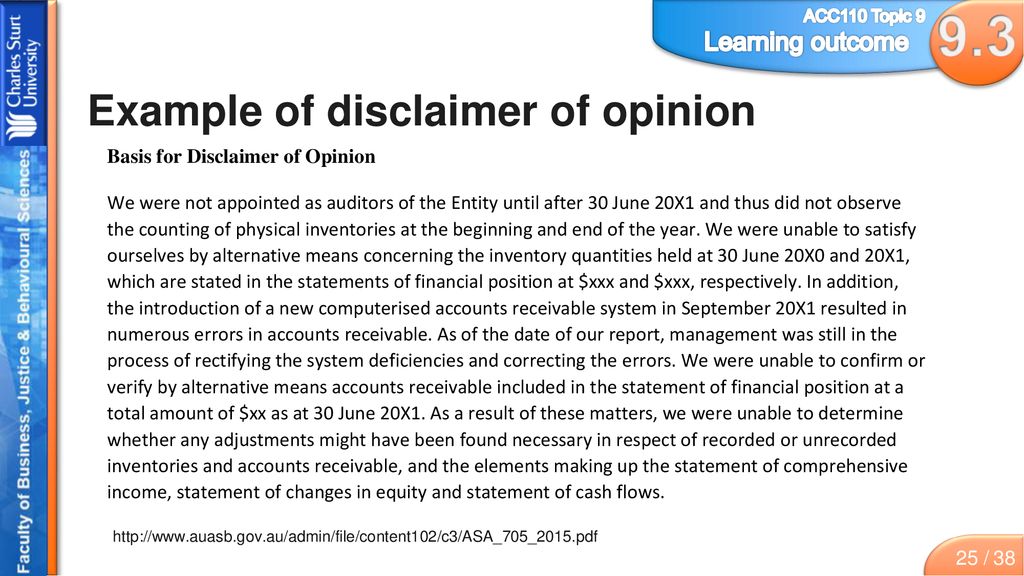

BERTAM ALLIANCE BERHAD BERTAM OR THE COMPANY DISCLAIMER OF OPINION ON THE AUDITED FINANCIAL STATEMENTS FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2019. Conclusions relating to going concern As the auditor has identified an issue that is so pervasive and is therefore unable to conclude on the financial statements as a whole it is not appropriate for the auditor to conclude on whether the use of the going concern basis of accounting is appropriate indeed the reason for the disclaimer. Auditor issues disclaimer of opinion on Viking Offshores FY18 statements raises going concern doubts.

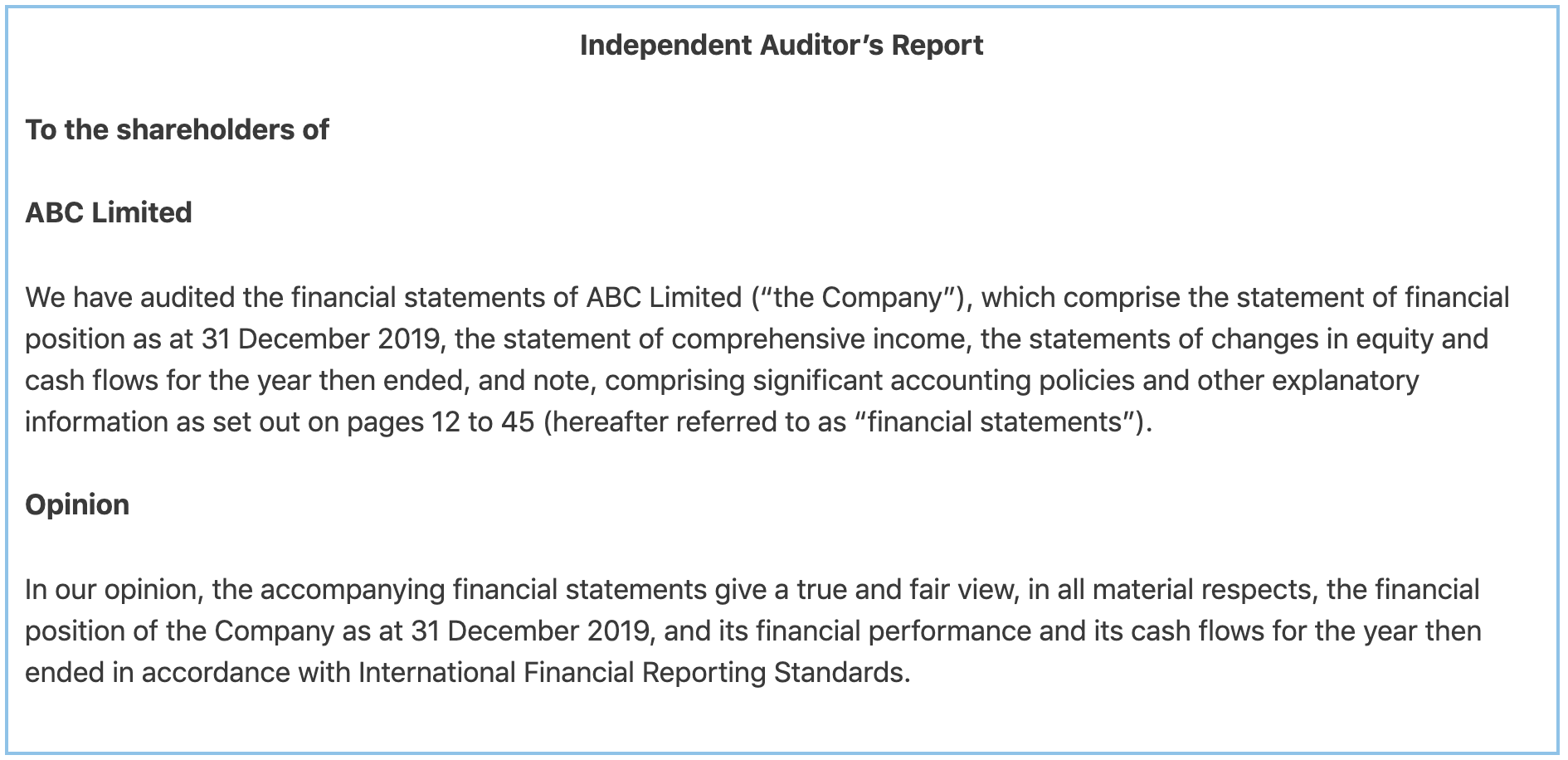

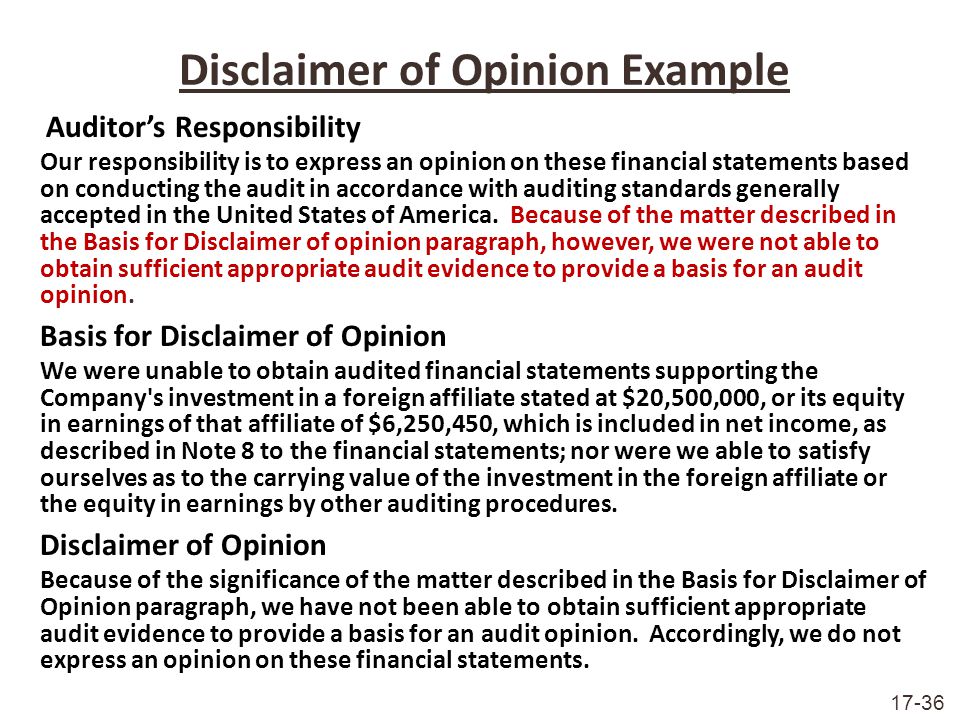

A disclaimer of opinion is issued when the auditor is unable to obtain sufficient appropriate audit evidence on which to base the opinion and the auditor concludes that the possible effects on the financial statements of undetected misstatements if any could be both material and pervasive. For now lets look at whats a Disclaimer Audit Opinion. Described in the Bases for Disclaimer of Opinion section of our report we have not been able to obtain sufficient appropriate audit evidence to provide a basis for an audit opinion on these financial statements.

Recently PWC Singapore issued Disclaimer Audit Opinion for its client Rickmers Maritime in view of the Groups uncertainties to continue as a going concern enity. Ability of the Company and the Group to repay debts when fall due. Continuity assumption is relevant for two di fferent types of.

There are material uncertainties that may cast significant doubt on the ability of the group and of the company to continue as going concerns Deloitte said in its report which was filed by TH Heavy to. AUDIT REPORT - MODIFIED OPINION MATERIAL UNCERTAINTY RELATED TO GOING CONCERN. The directors made representation that the disposal price has been revised downward from RMXXXXXXXX to RMXXXXXXXX.

Going Concern Profit And Loss Introduction Projection Excel

Https Isca Org Sg Media 2240868 Ssa 705r Nov 2018 Pdf Iso 14001 Audit Report Cash Flow Statement Of A Bank

Https Www Icaew Com Media Corporate Files Helpsheets Technical Aaf Guides Adverse Opinion Audit Report Ashx 3m Income Statement Normal Balance For Sales

Chapter 12 Auditors Reports The Very Existence Of Accounting Profession Depends On Public Confidence In Determination Certified Accountants Ppt Download Cash Flow From Financing Activities Meaning Ytd Profit And Loss

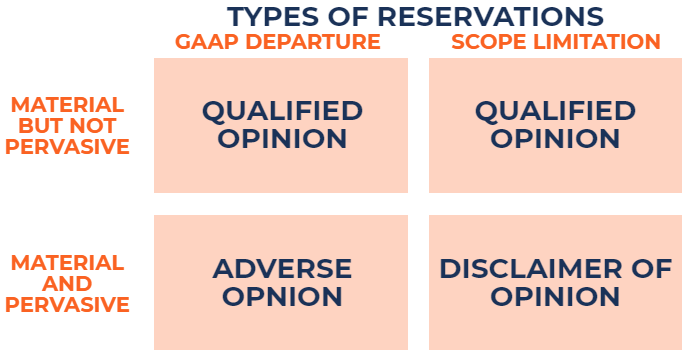

Auditor Opinions Overview Types Of Reservations Where Is Deferred Tax Asset In Balance Sheet Understanding The Cash Flow Statement

Going Concern Modifications And Related Disclosures In The Italian Stock Market Do Regulatory Improvements Help Investors Capturing Financial Distress Springerlink Comparative Contrast Essay Revenues On Balance Sheet

Https Cfrr Worldbank Org Sites Default Files 2020 03 12 Pdf Prepaid Rent Balance Sheet Classification Unconsolidated Financial Statements

Adverse Opinion Definition Example Vs Disclaimer Accountinguide Business Plan Trucking With Financial Projection Consolidated Comprehensive Income Statement